Post Office Monthly Income Scheme 2025 : A Complete Guide to Safe Monthly Returns

Everybody is looking for a low-risk investment plan that pays you every month. In that process, your search might be relevant and have taken you to the investment idea named the Post Office Monthly Income Scheme, which might be your ideal match in 2025.

The Post Office Monthly Income Scheme is a savings plan that is backed by the government, which pays guaranteed monthly interest on a lump sum investment. If you are looking for steady income without worrying much about the market volatility, then this can be the best monthly income choice for you. It is mostly favoured among the retirees, homemakers, as well as conservative investors who are looking for low risk as well as steady income.

Table of Contents

Interest Rate of Post Office Monthly Income Scheme 2025

As of May 2025, the interest of POMIS is around 7.4% per annum, which is payable monthly. For example, here is a table with an estimated financial projection..

| Investment Amount | Monthly Interest | Total in 5 Years |

| ₹1,00,000 | ₹616 | ₹36,960 |

| ₹5,00,000 | ₹3,083 | ₹1,84,980 |

| ₹9,00,000 (Max) | ₹5,550 | ₹3,33,000 |

Breakdown:

In the projection, the Rs 1,00,000 with 7.4% interest gives an overall monthly interest of Rs 616, which comes up to Rs 36,960 over the overall 5 years of time.

With Rs 5,00,000, the monthly interest becomes Rs 3,083, whereas in 5 years, it is projected to be Rs 1,84,980.

Rs 9,00,000 is the maximum limit of the account, which provides the monthly interest of Rs 5,550, whereas in total, over 5 years, it can reach up to Rs 3,33,000.

All the information given above is explicitly estimated, which may hinder the economic condition as well as the change in the inflation rate

Investment has different sides, perspectives, as well as goals to fulfill. This investment, particularly, has its own categorized goal where the individuals who are looking for only a stable income without any high risk are welcome to join the scheme. Stock provides an idea about significant growth with proper planning and strategy for the market value.

Why investing in the Post Office Monthly Income Scheme 2025 can be low-risk

The numbers of the values can change significantly based on economic demands, values, news, or any kind of action taking place within the organization. This can significantly influence the gains as well as the losses in the money. Investing in the post office’s monthly income scheme in 2025 provides an idea about stable monthly payouts without any stress about the fluctuation of the market, losing money, or strategically giving an idea about what stocks to buy.

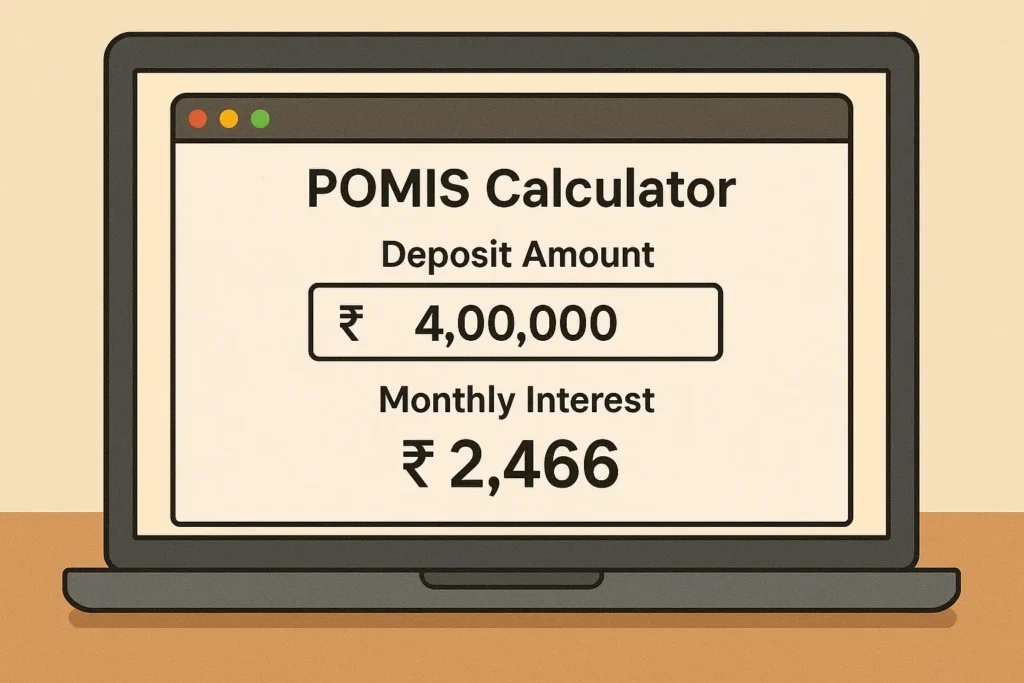

It is not always easier to understand the PMOIS amounts and other complex financials. If you want to plan better, use different POMIS calculators that are available on different sites such as Grow, ClearTax, or PolicyBazaar. Here you can enter your deposit, it will show your monthly income instantly.

Example:

For example, if you are investing Rs. 4 lakh, you will receive approximately Rs. 2,466 per month. This is going to help you with your fixed expenses, such as rent, EMI, or other utility bills, and help you in investment planning, while providing useful tools such as the post office monthly income scheme calculator.

Eligibility & Limits

- ✅ Minimum age: 10 years (minors allowed)

- ✅ Maximum investment: ₹9 lakh (individual), ₹15 lakh (joint)

- ✅ Tenure: 5 years

- ❌ NRIs are not eligible

How to Open an Account in the Post Office Monthly Income Scheme 2025

- Visit any India Post office.

- Submit Aadhaar, PAN, and a passport-size photo.

- Fill Form A and make the deposit via cheque/cash.

- Get your POMIS passbook instantly.

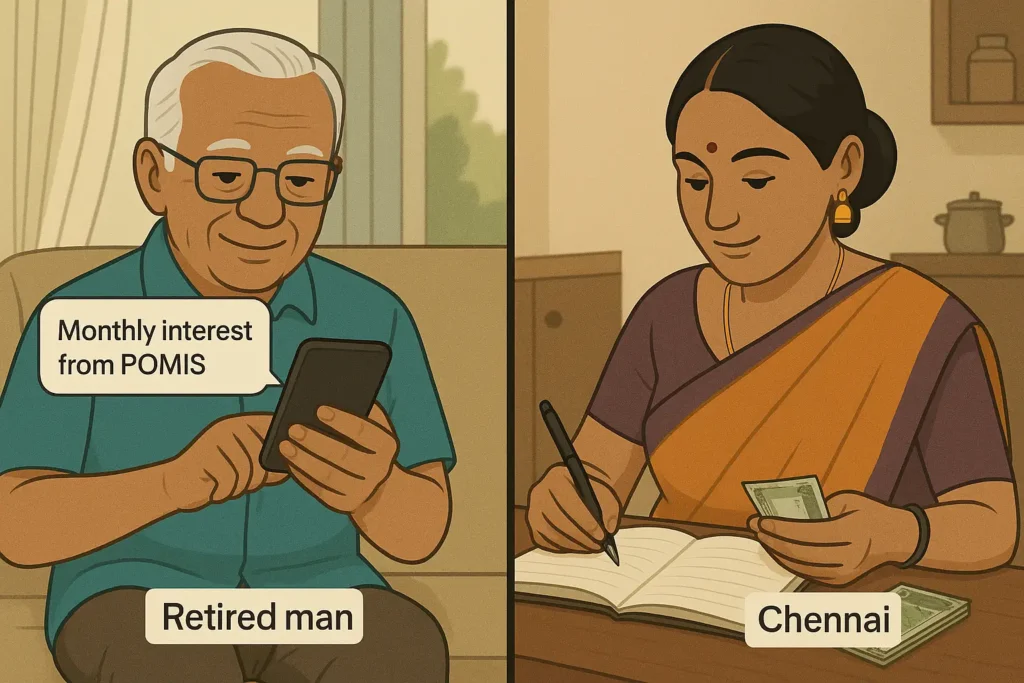

Example: Let me give you a practical scenario where Mr. Sharma is a retired LIC officer from Pune who has invested the maximum of Rs. 9 lakhs into his POMIS account. He receives around Rs. 5550 monthly as described in the chart, which helps him cover his health, insurance premiums, and other necessary needs. He also uses tax-saving ELSS funds to reduce his taxes on the interest.

Similarly, if another individual, such as a homemaker in Chennai, uses her lump sum of Rs. 3 lakhs in the POMIS monthly income scheme, it can help to earn a steady income of Rs. 1850 per month, which can be used for emergency funds or children’s education.

Comparison of different Investment plans

| Scheme | Interest | Tenure | Monthly Payouts | Tax Benefit? |

| POMIS | 7.4% | 5 yrs | Yes | No |

| SCSS (Senior) | 8.2% | 5 yrs | Quarterly | Yes (80C) |

| RBI Savings Bonds | 8.05% | 7 yrs | Half-yearly | No |

| HDFC Senior FD | 7.85% | 5 yrs | Yes | Yes |

| ICICI Monthly Income Plan (Mutual Fund) | Variable | Open-ended | Yes | Depends on capital gains |

- Calculate your HDFC Senior FD live, just select the time and “Yes” for senior.

- Calculate your ICICI Mutual Plan, and know more about the investment plan.

Tax Rules for 2025

- Interest is taxable under “Income from Other Sources.”

- No TDS deducted

- File ITR if total interest exceeds limits (₹40,000 for general, ₹50,000 for seniors)

- No deductions under 80C

Reinvestment Options After 5 Years

When POMIS matures:

- Reinvest in a new POMIS cycle

- Move to SCSS (if 60+)

- Shift to low-risk mutual funds like HDFC Hybrid Equity

- Consider bank FDs with higher rates

- Use as capital for a side business or a real estate deposit

Pros & Cons

Pros:

- Government backed

- Fixed monthly income

- No market risk

Cons:

- Not inflation-linked

- Returns are taxable

- Offline process (as of 2025)

*DO NOT FORGET TO FILE YOUR ITR

Conclusion

Having a reliable investment and income that pays you monthly is a dream of many households in India. As of 2025, the post office monthly income scheme 2025 provides a smart investment choice for individuals who remain risk-averse investors as well as seeking monthly payouts rather than a great fluctuations.

Frequently Asked Questions (FAQs)

1. What is the maximum investment in the Post Office Monthly Income Scheme in 2025?

As of May 2025, the maximum allowed investment is ₹9 lakh for a single account and ₹15 lakh for a joint account.

2. Is POMIS interest tax-free?

No. Interest earned is taxable under “Income from Other Sources.” However, there’s no TDS.

3. Can NRIs invest in POMIS?

No, NRIs are not eligible to invest in this scheme.

4. Can I open multiple POMIS accounts?

Yes, but the total investment across all accounts must not exceed the maximum limit.

5. Can I withdraw my money early?

Yes, premature withdrawal is allowed after 1 year. Penalties apply: 2% deduction if withdrawn before 3 years, 1% if after 3 years.

6. Can I open a POMIS account online?

As of 2025, POMIS can only be opened offline at India Post branches. However, India Post is testing digital services.

7. Is the POMIS interest credited to a savings account?

Yes, the monthly interest can be credited to a linked post office savings account or ECS to your bank account.

You May Also Like